The Scalability Signal: When Pharma Pounces

Why platform technologies may be the scale engine biotech's been waiting for

Hi! I’m Cristina. With roots in science and a track record leading strategy and partnerships across biotech, I focus on one thing: identifying breakthroughs that will make cell therapies mainstream—and invest before the world catches on.

Well, I guess this is becoming a thing! In my last post, I opened up about how writing doesn’t come naturally but your kind encouragement meant a lot, so I’m sticking with it (and having a bit of fun with it too). Thanks for helping me keep the momentum!

For the past year, I’ve been digging into a hypothesis that I just can’t shake: platform technologies that solve scalability challenges in cell therapy still hold powerful appeal for large pharma, even in a tough and unpredictable macro environment. This post is my take on why that’s happening, and why the right platform at the right time still commands capital, attention, and long-term strategic bets.

A quick note before diving: for the sake of simplicity, I’m using “Gene Therapy” and “Cell Therapy” interchangeably here. I see Gene Therapy as a type of Cell Therapy, since the ultimate target of the intervention is the cell.

How Big Pharma Got BIG?

I recently came across a fascinating story about how one Big Pharma became, well, big, and I’d love to share it here.

It all started back in 1928, when Alexander Fleming returned from vacation to find a petri dish he’d accidentally left out covered in mold. Fleming noticed that the mold seemed to be killing the surrounding bacteria, and what followed was the discovery of penicillin, often called “the single greatest victory ever achieved over disease.” Before penicillin, even minor infections like strep throat or a scraped knee could be fatal. Surgery was a gamble. If you survived, it was pure luck.

And yet, even after Fleming’s discovery, penicillin wasn’t immediately useful because no one knew how to extract it from the mold or mass produce it. At the beginning of World War II, bacterial infections were the leading cause of death for wounded soldiers. That is, until the U.S. government challenged a little-known chemical company called Pfizer.

Pfizer jumped at the challenge. By D-Day in 1944, Pfizer had produced enough penicillin to treat every allied soldier wounded in the invasion using their deep tank fermentation industrial technology. By the end of the war, Pfizer was cranking out 650 billion units per month, a feat that catapulted this once-small chemical company into the global pharmaceutical giant it is today. Even today, penicillin is a $10B global market [Fun fact: I’m allergic to penicillin, so I’ve contributed exactly $0].

Pfizer’s rise to global prominence is a fascinating tale, but it’s far from unique. In fact, it’s the story of how most “Big Pharma” made their mark: by solving scalability challenges. Let me share two other interesting examples: Genentech (Roche) pioneered the use of recombinant DNA to produce insulin. Before the 1980s, it took the pancreas of about 50 pigs to produce enough insulin for just one diabetic patient per year! (talk about supply chain challenge :-)). Amgen figured out how to scale up the production of complex biologics through its investments in cell line development, resulting in a string of blockbuster drugs.

The examples above are just a few, there are others that have paved the way for the industry. The common thread? they didn’t just solve scientific problems. They solved scalability.

The TAM Obsession: Not just a VC Thing

We often think of TAM (Total Addressable Market) as VC territory but drug developers are just as hooked [Fun fact: in consumer tech, TAM is often irrelevant, who knew we needed Uber, Airbnb or an iPhone?].

TAM isn’t just a theoretical exercise, it’s rather a lens into what matters most to a drug developer. How a company calculates TAM reveals its internal compass. And that starts with a deceptively simple question: Who’s the real customer?

“We will continue to focus relentlessly on our customers” Jeff Bezos, Letter to Shareholders (1997)

A lively debate broke out over lunch the other day with some friends in my circle: Who’s the customer in a drug development company? Most people usually land somewhere between “the patient”, “the doctor”, and the “payor”. I used to be firmly in the payor camp (they hold the purse strings, after all). But the more I think about it, the more I realize that the real answer is complicated. In drug development there’s a whole chain of people who have to say yes: regulators need to approve, doctors need to prescribe, payors need to reimburse and patients need to actually want or need the treatment. That said, most drug developers act on one big assumption: if there’s a true unmet medical need, doctors will prescribe, and payors will pay. Which is why, in practice, TAM if often calculated as: # eligible patients x price per treatment.

To avoid sparking a dinner party debate on drug pricing, let’s focus on the human side of the equation: the eligible patients. Drug developers are obsessed with finding and reaching as many of them as possible. That’s all they talk about and that’s why nearly every biotech and Big Pharma mission statement you read includes the words “the patient”. The end goal is always: reach more patients (so maybe the patient is the end customer?).

Big Pharma, in particular, is obsessed with removing bottlenecks to production because they can treat more people. And if you look closely, some of the largest pharma acquisitions in recent years weren’t about hot science, they were about solving for scale. That’s not a coincidence. That’s strategy.

Why Scale Still Wins

Before we dive into recent M&A trends, let’s pause on a simple but powerful concept: economies of scale. In its classic form, it refers to the cost advantage a company enjoys as it increases output. Fixed costs get spread across more programs, and operations become more efficient with repetition. That’s the textbook answer. But let’s bring it back to Big Pharma. How do they actually scale? Historically, it’s through shared manufacturing, centralized teams, drug repurposing and increasingly, platform technologies. Of these levers, platforms may be the most underappreciated and arguably one of the most powerful. Few assets can do so much heavy lifting across an entire pipeline.

As it core, a platform is a repeatable, scalable innovation engine. In drug development, a platform is a scientific or technical capability that can be applied across multiple therapeutic areas, disease targets, or drug modalities. When it works, it transform the economics: a single platform can generate an entire pipeline, streamline production, reduce cost, improve reproducibility, and dramatically accelerate time to clinic.

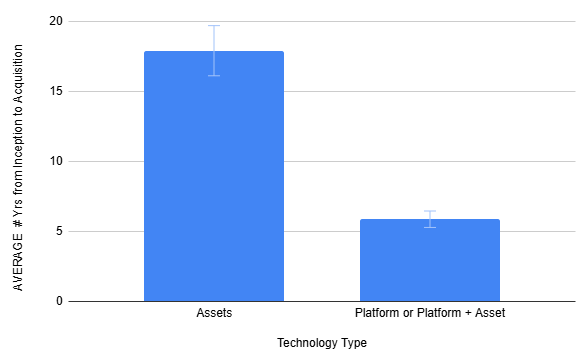

If you’ve been following recent M&A trends, you’ve probably noticed it too: consistent interest in early-stage, platform-centric deals (see below). While the common narrative attributes acquisitions to the looming patent cliffs and the need to backfill near-term revenue, that data tells a different story. Many recent deals involved no late-stage, de-risked assets. Instead, Big Pharma went upstream for platforms. Sure, you could argue that this trend is partly a function of scarcity. But I believe what’s really happening is future differentiation driven by new engines to make drugs.

Side bonus, platform technologies seem to be exiting faster, with attractive multiples (see above and below).

Purpose Meets Profit: The Case for Cell Therapies

Now, back to cell therapies before we spiral into another dinner-party debate on valuations😉. The promise is real and Big Pharma knows it. That’s why 13 out of the top 15 players have already made moves in the space. From the inside, we all see the same hurdles: it’s still too complex, too costly, and too slow. But, platforms that reduce cost, simplify workflows, and enable scale are handsomely rewarded.

Cell therapies have shown remarkable clinical potential in recent years, with a steady drumbeat of approvals and a higher probability of success once in trials. When platforms are disease-agnostic (spanning cancer, neurodegeneration, genetic disorders, and more), the value they can unlock becomes exponential. That’s why acquisitions like Gracell, EsoBiotec, and Kate weren’t flukes. They were calculated moves backed by deep conviction in scalable platforms. But here’s the rub: for all the buzz, truly scalable platforms are rare. Many overpromise. Few can actually deliver the reproducibility and manufacturing readiness that the field demands. I believe we’re just at the beginning of this wave and the most valuable companies are still flying under the radar.

If you’re tracking the space, keep an eye on these categories of platform tech:

In vivo targeted delivery (both viral and non-viral),

Off-the-shelf solutions,

<1-day manufacturing or bedside manufacturing, and last but not least:

Automation (yes, AI and robots!)

I’ve got my favorite startups in each bucket and happy to trade notes if you’re tracking this space too!

If this sparked any ideas or nudge your thinking, I’d love to hear where you think the field heading. And if you’re looking for deeper takes or warm intros to operators and founders building in this space, just say the word!